Advertising:

2000 Chrysler Concorde Lx on 2040-cars

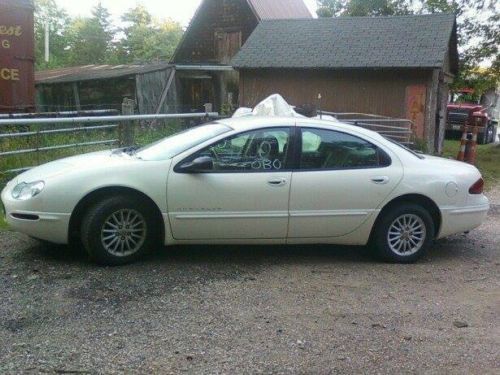

US $2,750.00

Year:2000

Mileage:160193

Color:

Location:

969 N Range Line Rd, Carmel, Indiana, United States

Fuel Type:Gasoline

Engine:2.7L V6 24V MPFI DOHC

Transmission:4-Speed Automatic

Engine:2.7L V6 24V MPFI DOHC

Transmission:4-Speed Automatic

Condition: Used

VIN (Vehicle Identification Number): 2C3HD46RXYH156322

Stock Num: EV-156322

Make: Chrysler

Model: Concorde LX

Year: 2000

Exterior Color: Shale Green Metallic

Interior Color: Gray

Options: Drive Type: FWD

Number of Doors: 4 Doors

Mileage: 160193

VIN (Vehicle Identification Number): 2C3HD46RXYH156322

Stock Num: EV-156322

Make: Chrysler

Model: Concorde LX

Year: 2000

Exterior Color: Shale Green Metallic

Interior Color: Gray

Options: Drive Type: FWD

Number of Doors: 4 Doors

Mileage: 160193

Please contact dealer to verify price options and other vehicle details.

Chrysler Concorde for Sale

2003 chrysler concorde limited(US $5,980.00)

2003 chrysler concorde limited(US $5,980.00) 1999 chrysler concorde lx(US $3,994.00)

1999 chrysler concorde lx(US $3,994.00) 1997 chrysler concorde lxi(US $5,944.00)

1997 chrysler concorde lxi(US $5,944.00) 2003 chrysler concorde lxi(US $4,500.00)

2003 chrysler concorde lxi(US $4,500.00) 2004 chrysler concorde lxi(US $2,695.00)

2004 chrysler concorde lxi(US $2,695.00) 2001 chrysler concorde lx sedan 4-door 3.2l

2001 chrysler concorde lx sedan 4-door 3.2l

Auto Services in Indiana

Zips Auto Repair ★★★★★

Auto Repair & Service

Address: 388 S B St, Scipio

Phone: (513) 867-9722

West Coliseum Auto Sales ★★★★★

New Car Dealers, Used Car Dealers, Wholesale Used Car Dealers

Address: 1029 W Coliseum Blvd, Laotto

Phone: (260) 484-6100

WE Are Auto Care ★★★★★

Auto Repair & Service, Automobile Inspection Stations & Services, Automobile Diagnostic Service

Address: 101 N State Road 57, Washington

Phone: (812) 254-2950

Van Winkle Service Center ★★★★★

Auto Repair & Service, Tire Dealers, Auto Oil & Lube

Address: 1529 Highway 64 NW, Ramsey

Phone: (812) 347-3134

Stoops Buick GMC ★★★★★

Auto Repair & Service, New Car Dealers, Automobile Body Repairing & Painting

Address: 4055 W Clara Ln, Oakville

Phone: (765) 273-6904

Staples Pipe & Muffler ★★★★★

Automobile Parts & Supplies, Mufflers & Exhaust Systems, Automobile Accessories

Address: 523 Hoosier St, Vernon

Phone: (812) 346-2474

Auto blog

Federal judge throws out GM's racketeering lawsuit against Fiat Chrysler

Thu, Jul 9 2020Â DETROIT — A federal judge on Wednesday threw out a racketeering lawsuit General Motors had filed against smaller rival Fiat Chrysler Automobiles, saying the No. 1 U.S. automaker's alleged injuries were not caused by FCA's alleged violations. GM officials said in statement they "strongly disagree" with the order by U.S. District Court Judge Paul Borman, whom the automaker had sought to have removed from the case, and would appeal. "There is more than enough evidence from the guilty pleas of former FCA executives to conclude that the company engaged in racketeering, our complaint was timely and showed in detail how their multi-million dollar bribes caused direct harm to GM," GM said in a statement. The Detroit company added that Borman's decision "would let wrongdoers off the hook." GM filed the racketeering lawsuit against FCA last November, alleging its rival bribed United Auto Workers (UAW) union officials over many years to corrupt the bargaining process and gain advantages, costing GM billions of dollars. GM was seeking "substantial damages" that one analyst said could have totaled at least $6 billion. FCA had called the case meritless and asked Borman to dismiss it. On Wednesday, Borman dismissed the lawsuit "with prejudice," meaning GM cannot refile the complaint. "The direct victims of defendants' alleged bribery scheme are FCA's workers," Borman wrote of FCA. "GM's high labor costs were not an injury proximately caused by FCA's bribes, and any competitive injury that GM suffered as a result of FCA's advantage in labor costs is an indirect injury." "The dismissal of GM's complaint with prejudice earlier today vindicates our position," FCA said in a statement. On Monday, the Sixth U.S. Circuit Court of Appeals denied GM's petition to remove Borman from the case, but said the two automakers' chief executives didn't have to meet to try to settle the case as Borman had ordered. In calling for that, Borman had called the lawsuit "a waste of time and resources." Â Government/Legal UAW/Unions Chrysler Fiat GM

Why this could be the perfect time for Apple to make a car play

Fri, Aug 31 2018While the automotive and technology worlds have been pouring billions into autonomous vehicles (AVs) and preparing to bring them to market soon as shared robo-taxis, Apple has mostly sat on the sidelines. Of course, Apple is the last company to ever make its intentions known, and the super-secret tech cult giant hasn't been totally out of the AV game based on the clues that have slipped out of its Cupertino, Calif., citadel over the past few years. Related: Apple self-driving cars are real — one was just in an accident News first broke in 2015 that it had assembled an automotive development team, in part by poaching high-profile talent from car companies, to work on a top-secret self-driving vehicle project code-named Titan. (Thank you very much, Nissan.) Apple also subsequently broke cover by making inquiries into using a Northern California AV testing facility and receiving a permit to test AVs on public roads in California. But then as the AV race started to heat up in the last few years, Apple reportedly began scaling back its car activities by downsizing team Titan. More recently, Apple's car project has shown signs of life with the hiring a high-level engineer away from Waymo and luring one Tesla's top engineers and a former employee back to Apple. It also inked a deal with Volkswagen to provide a technology platform and software to convert the automaker's new T6 Transporter vans into autonomous shuttles for employees at tech company's new campus. That is a far cry from giving rides to Wal-Mart shoppers, like Waymo is doing as part of its AV testing in Phoenix. But this could be the perfect time for Apple to enter the AV market now that ride-sharing is reaching critical mass and automakers and others are planning to deploy fleets of robo-taxis. Apple could easily establish a niche as a high-end ride-sharing service – and charge a premium – given its cult-like brand loyalty and design savvy. The growth of car subscription models could also play in Apple's favor since is already has many people hooked on paying for phones in monthly installments – and eager to upgrade when a new and better model becomes available. To achieve this, some believe Apple will fulfill co-founder and CEO Steve Job's dream of building a car. And as the world's first and only $1 trillion company it's sitting on a mountain of cash that certainly gives it the means. But other tech darlings like Tesla and Google have discovered how difficult it can be to build cars at scale.

Weekly Recap: Chrysler forges ahead with new name, same mission

Sat, Dec 20 2014Chrysler is history. Sort of. The 89-year-old automaker was absorbed into the Fiat Chrysler Automobiles conglomerate that officially launched this fall, and now the local operations will no longer use the Chrysler Group name. Instead, it's FCA US LLC. Catchy, eh? Here's what it means: The sign outside Chrysler's Auburn Hills, MI, headquarters says FCA (which it already did) and obviously, all official documents use the new name, rather than Chrysler. That's about it. The executives, brands and location of the headquarters aren't changing. You'll still be able to buy a Chrysler 200. It's just made by FCA US LLC. This reinforces that FCA is one company going forward – the seventh largest automaker in the world – not a Fiat-Chrysler dual kingdom. While the move is symbolic, it is a conflicting moment for Detroiters, though nothing is really changing. Chrysler has been owned by someone else (Daimler, Cerberus) for the better part of two decades, but it still seemed like it was Chrysler in the traditional sense: A Big 3 automaker in Detroit. Now, it's clearly the US division of a multinational industrial empire; that's good thing for its future stability, but bittersweet nonetheless. Undoubtedly, it's an emotion that's also being felt at Fiat's Turin, Italy, headquarters as the company will no longer officially be called Fiat there. Digest that for a moment. What began in 1899 as the Societa Anonima Fabbrica Italiana di Automobili Torino – or FIAT – is now FCA Italy SpA. In a statement, FCA said the move "is intended to emphasize the fact that all group companies worldwide are part of a single organization." The new names are the latest changes orchestrated by CEO Sergio Marchionne, who continues to makeover FCA as an international automaker that has ties to its heritage – but isn't tied down by it. Everything from the planned spinoff of Ferrari, a new FCA headquarters in London and the pending demise of the Dodge Grand Caravan in 2016 has shown that the company is willing to move quickly, even if it's controversial. While renaming the United States and Italian divisions were the moves most likely to spur controversy, FCA said other regions across the globe will undergo similar name changes this year. Despite the mixed emotions, it's worth noting: The name of the merged company that oversees all of these far-flung units is Fiat Chrysler Automobiles. Obviously the Chrysler corporate name isn't completely history.